import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from pandas.plotting import register_matplotlib_converters

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

register_matplotlib_converters()

import os

data_folder = '../data/'

1: ACF vs PACF#

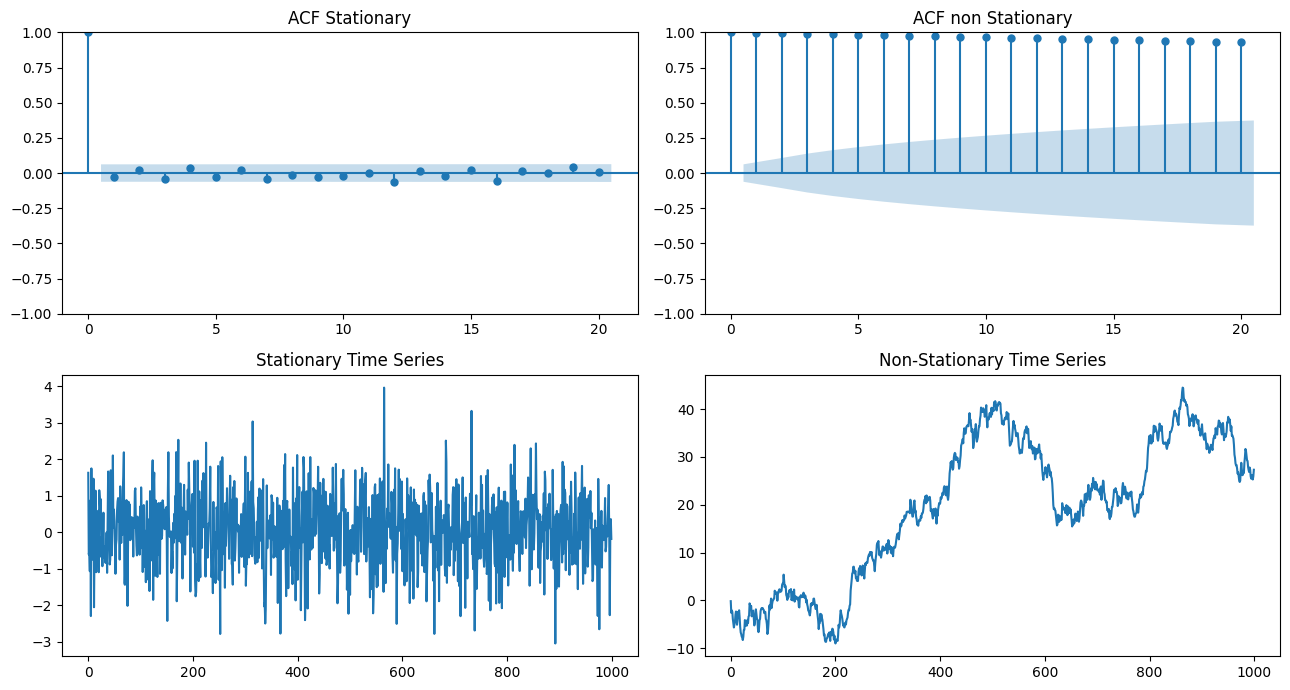

# Generate a stationary time series

np.random.seed(1)

stationary_ts = np.random.normal(0, 1, size=1000)

# Generate a non-stationary time series

nonstationary_ts = np.cumsum(np.random.normal(0, 1, size=1000))

# Compute the autocorrelation function for both time series

lags = 20

plt.subplots(2, 2, figsize=(13,7))

acf_stationary = plot_acf(stationary_ts, lags=lags, alpha=0.05, ax=plt.subplot(221), title='ACF Stationary')

acf_nonstationary = plot_acf(nonstationary_ts, lags=lags, alpha=0.05, ax=plt.subplot(222), title= 'ACF non Stationary')

# Plot the time series

plt.subplot(223)

plt.plot(stationary_ts)

plt.title("Stationary Time Series")

plt.subplot(224)

plt.plot(nonstationary_ts)

plt.title("Non-Stationary Time Series")

plt.tight_layout()

plt.show()

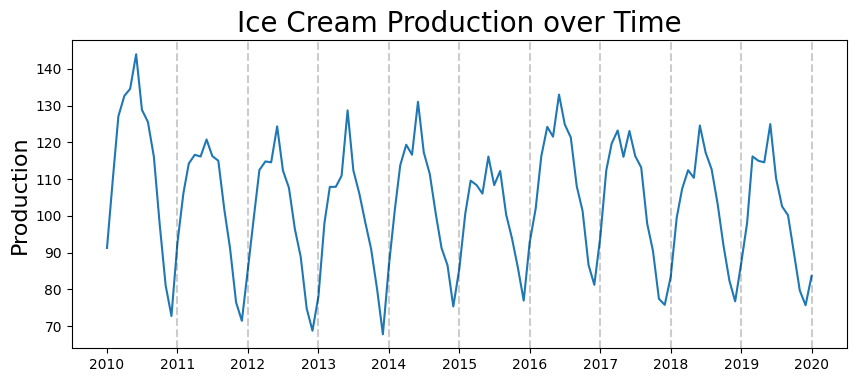

Ice Cream Production Data#

#read data

df_ice_cream = pd.read_csv(os.path.join(data_folder, 'ice_cream.csv'))

df_ice_cream.head()

| DATE | IPN31152N | |

|---|---|---|

| 0 | 1972-01-01 | 59.9622 |

| 1 | 1972-02-01 | 67.0605 |

| 2 | 1972-03-01 | 74.2350 |

| 3 | 1972-04-01 | 78.1120 |

| 4 | 1972-05-01 | 84.7636 |

#rename columns to something more understandable

df_ice_cream.rename(columns={'DATE':'date', 'IPN31152N':'production'}, inplace=True)

#convert date column to datetime type

df_ice_cream['date'] = pd.to_datetime(df_ice_cream.date)

#set date as index

df_ice_cream.set_index('date', inplace=True)

#just get data from 2010 onwards

start_date = pd.to_datetime('2010-01-01')

df_ice_cream = df_ice_cream[start_date:]

#show result

df_ice_cream.head()

| production | |

|---|---|

| date | |

| 2010-01-01 | 91.2895 |

| 2010-02-01 | 110.4994 |

| 2010-03-01 | 127.0971 |

| 2010-04-01 | 132.6468 |

| 2010-05-01 | 134.5576 |

plt.figure(figsize=(10,4))

plt.plot(df_ice_cream.production)

plt.title('Ice Cream Production over Time', fontsize=20)

plt.ylabel('Production', fontsize=16)

for year in range(2011,2021):

plt.axvline(pd.to_datetime(str(year)+'-01-01'), color='k', linestyle='--', alpha=0.2)

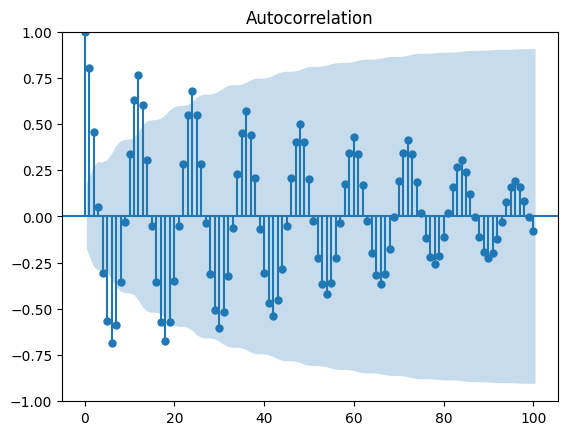

ACF#

acf_plot = plot_acf(df_ice_cream.production, lags=100)

Based on decaying ACF, we are likely dealing with an Auto Regressive process#

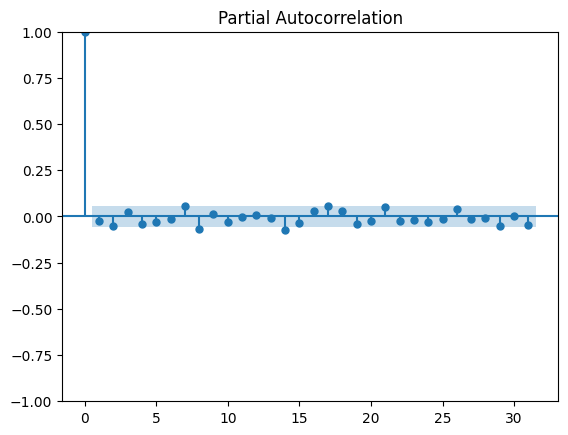

PACF#

pacf_plot = plot_pacf(df_ice_cream.production)

/home/ubuntu/Documents/Projects/STI_FX_Intervention/.venv/lib/python3.9/site-packages/statsmodels/graphics/tsaplots.py:348: FutureWarning: The default method 'yw' can produce PACF values outside of the [-1,1] interval. After 0.13, the default will change tounadjusted Yule-Walker ('ywm'). You can use this method now by setting method='ywm'.

warnings.warn(

Based on PACF, we should start with an Auto Regressive model with lags 1, 2, 3, 10, 13#

On stock data#

import yfinance as yf

#define the ticker symbol

tickerSymbol = 'SPY'

#get data on this ticker

tickerData = yf.Ticker(tickerSymbol)

#get the historical prices for this ticker

tickerDf = tickerData.history(period='1d', start='2015-1-1', end='2020-1-1')

tickerDf = tickerDf[['Close']]

#see your data

tickerDf.head()

| Close | |

|---|---|

| Date | |

| 2015-01-02 00:00:00-05:00 | 176.788849 |

| 2015-01-05 00:00:00-05:00 | 173.596115 |

| 2015-01-06 00:00:00-05:00 | 171.961029 |

| 2015-01-07 00:00:00-05:00 | 174.103851 |

| 2015-01-08 00:00:00-05:00 | 177.193390 |

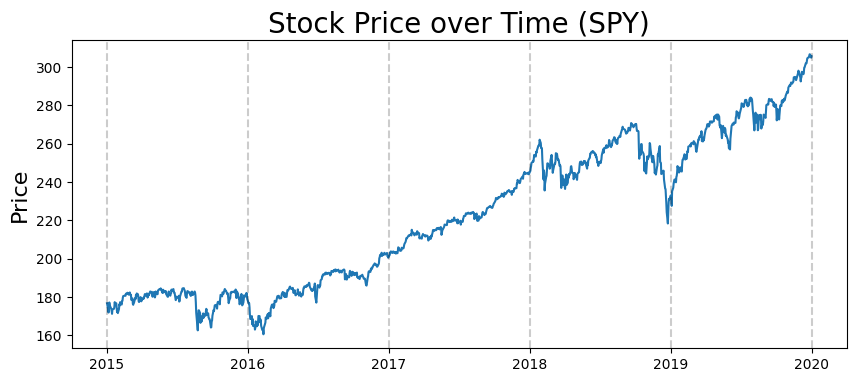

plt.figure(figsize=(10,4))

plt.plot(tickerDf.Close)

plt.title('Stock Price over Time (%s)'%tickerSymbol, fontsize=20)

plt.ylabel('Price', fontsize=16)

for year in range(2015,2021):

plt.axvline(pd.to_datetime(str(year)+'-01-01'), color='k', linestyle='--', alpha=0.2)

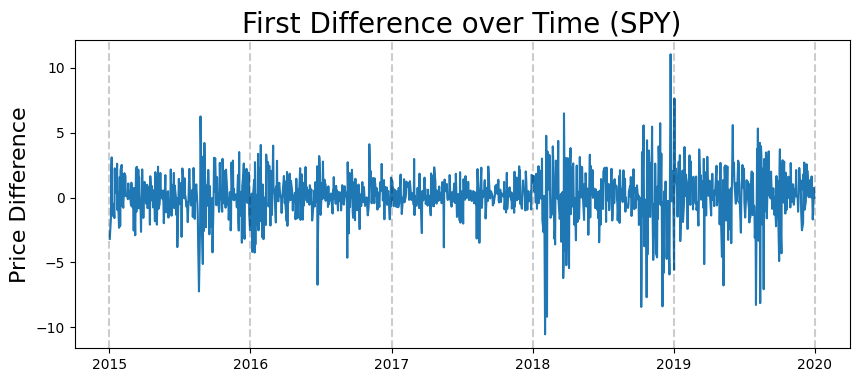

Stationarity: take first difference of this series#

#take first difference

first_diffs = tickerDf.Close.values[1:] - tickerDf.Close.values[:-1]

first_diffs = np.concatenate([first_diffs, [0]])

#set first difference as variable in dataframe

tickerDf['FirstDifference'] = first_diffs

tickerDf.head()

| Close | FirstDifference | |

|---|---|---|

| Date | ||

| 2015-01-02 00:00:00-05:00 | 176.788849 | -3.192734 |

| 2015-01-05 00:00:00-05:00 | 173.596115 | -1.635086 |

| 2015-01-06 00:00:00-05:00 | 171.961029 | 2.142822 |

| 2015-01-07 00:00:00-05:00 | 174.103851 | 3.089539 |

| 2015-01-08 00:00:00-05:00 | 177.193390 | -1.419983 |

plt.figure(figsize=(10,4))

plt.plot(tickerDf.FirstDifference)

plt.title('First Difference over Time (%s)'%tickerSymbol, fontsize=20)

plt.ylabel('Price Difference', fontsize=16)

for year in range(2015,2021):

plt.axvline(pd.to_datetime(str(year)+'-01-01'), color='k', linestyle='--', alpha=0.2)

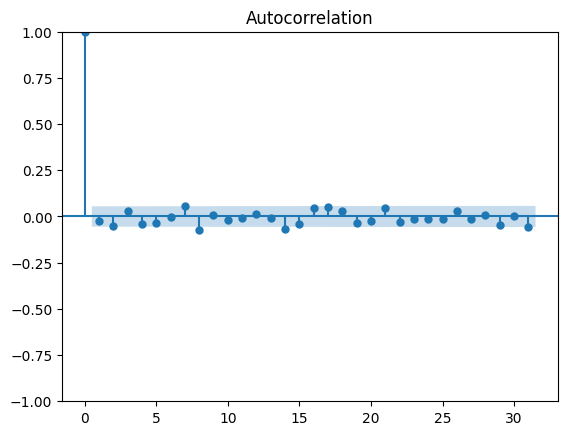

ACF#

acf_plot = plot_acf(tickerDf.FirstDifference)

ACF isn’t that informative#

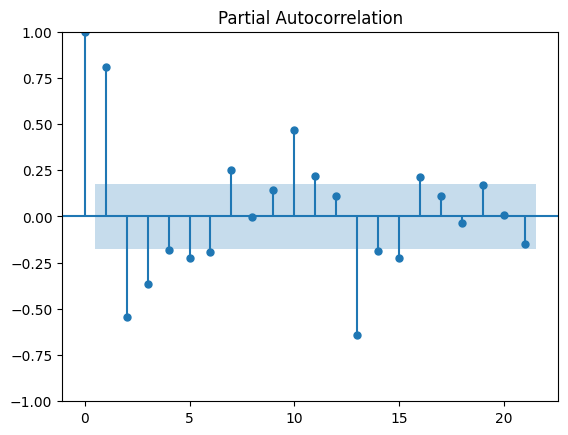

PACF#

pacf_plot = plot_pacf(tickerDf.FirstDifference)

/home/ubuntu/Documents/Projects/STI_FX_Intervention/.venv/lib/python3.9/site-packages/statsmodels/graphics/tsaplots.py:348: FutureWarning: The default method 'yw' can produce PACF values outside of the [-1,1] interval. After 0.13, the default will change tounadjusted Yule-Walker ('ywm'). You can use this method now by setting method='ywm'.

warnings.warn(